Few states have done as much as Massachusetts (MA) over the last 30 years to lower healthcare costs, improve quality and outcomes and, in general, to innovate.

Last week the MA Health Policy Commission issued its 2019 Annual Health Care Cost Trends Report documenting wins, losses, and opportunities for change. Romney Care was passed in 2006 and, in 2012, the state passed a sweeping initiative to focus on a healthcare growth target and transparent metrics for evaluating healthcare performance statewide.

Despite significant initiatives, the state reports slippage in many metrics, including burdensome cost increases for employers and their employees.

The report points to issues that now vex healthcare policy makers in every state, including medical debt burden, unaffordable premiums and cost shift to employees through plan design and premium share.

Further, the report calls for employers to get off the sidelines and to actively “work collaboratively toward [making the marketplace] a more high value system.“ Massachusetts provides some of the best healthcare at close to the highest costs in the nation.

In MA, six hospital systems dominate the market. Quality and cost of care are MA’s biggest challenges, just as they are nationwide. Some fascinating statistics:

- Commercial inpatient volume decreased by 9.3% between 2014-18 but spending per inpatient stay grew 5.2% annually between 2013 and 2018, from $14,500 to $18,700. Hospitals have become adept at upcoding or increasing acuity and patient risk scores. These increased by 11.7% during the same period.

- "Hospital readmissions rate in MA is higher than nearly every state in the US."

- "Payments per major outpatient surgery episode were nearly twice as high at Mass General Hospital and Brigham as the lowest-paid high-volume hospital.”

- Despite decreasing volumes, hospitals are charging more and using technology to leverage risk scores for bigger compensation opportunities.

- The biggest hospital systems are winning while community hospitals continue to get less volume.

Who pays for all this? Employers and their employees bear much of the burden for these increased costs. Other key findings from the report:

- "Health care spending growth in MA between 2016-18 absorbed almost 40 cents of every additional [dollar] earned for families with coverage through employers, more than they took home in pay after taxes."

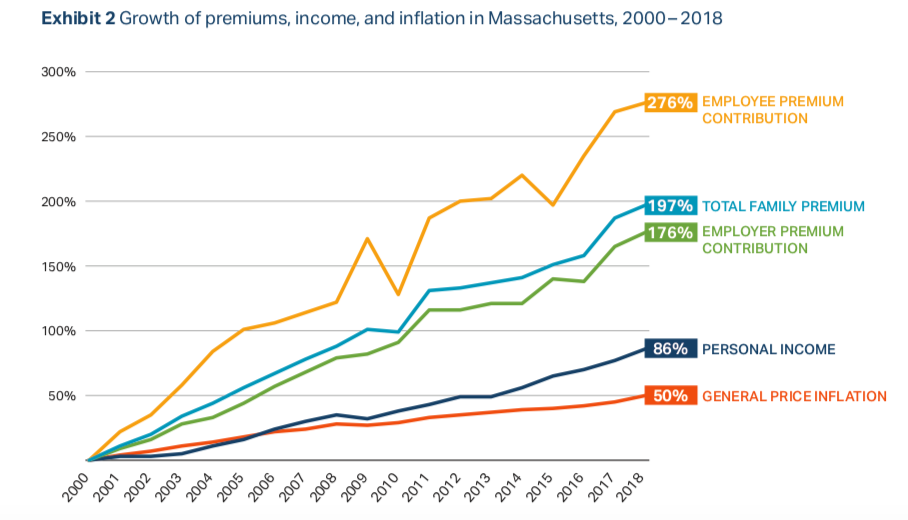

- "Between 2000 and 2018 in MA, the Consumer Price Index (CPI) grew by 50%, while the average cost for a family premium nearly tripled, from $7,341 to $21,801. Employees direct premium contributions rose even faster - by a factor of nearly four - as employees paid an increasingly larger share of premiums over this time period out of their paychecks (increasing from 21 percent of the premium being paid by employees to 26%)."

- "In 2017, one in four MA residents reported having gone without needed medical or dental care due to cost, and 17% reported having family medical debt. In 2019, one in four MA residents reported forgoing medically necessary prescription drugs...

Employees are bearing the burden for increased costs, and are increasingly unable to pay for necessary medical services. This isn’t a promising trajectory.

The report covers many issues that most of us see everyday, including inadequate primary care and behavioral health attribution, lack of adequate ambulatory care access and steerage, out-of-control pharmacy spending and opaque pricing, facility fees, low value care, provider pricing variation and out-of-network billing.

Perhaps one of the most disconcerting findings in the report relates to Alternative Payment Methods (APMs) and provider risk arrangements. The report has an excellent accompanying chartpak that looks at these. In areas that feature many contracted providers utilizing upside/downside risk arrangements, employers generally benefit. These arrangements often protect the employer and employees from costs borne by providers (complications and infections) as part of the arrangement.

Other takeaways from the report:

- “The percent of members in global full payment arrangements decreased from 35.3% in 2016 to 31.5% in 2018.”

- “The overall rate of APM adoption across all products in MA declined from 45% in 2016 to 42% in 2018.” This is truly remarkable. We see other states making progress, influencing providers to move to Alternative Payment Methods which require provider risk and quality outcomes. The bottom line is that APMs hold providers directly accountable for the care they provide to patients via attribution. APM slippage is a negative trend.

So, in the face of apparent slippage, who does the state want to become more involved? As part of the 2019 Summary Policy Recommendations in the report there is a very clear recommendation for employer engagement and consumer choice. This recommendation appears repeatedly in the report, and is a call to arms, so to speak, for the Massachusetts business community:

“Employer Engagement and Consumer Choice. The Massachusetts business community should increase its coordinated engagement to drive changes in health care. Employers should collaborate with payers, providers, and other stakeholders to influence changes in spending and affordability, care delivery, and the promotion of a value-based market.”

The recommendation goes on to suggest the promotion of “two sided contracts.”

Massachusetts policymakers and others have worked hard over a thirty year period to push for healthcare innovation, access and accountability.

Massachusetts boasts the lowest rate of uninsured residents in the US. At the same time, MA also experiences many of the same problems that plague other states. Employers and employees continue to bear the burden for ever increasing hospital and drug costs, and progress with APMs has apparently stalled or reversed.

Will employers seize the day and demand change? Will benefits brokers and consultants finally be held responsible by employers in favor of value-based arrangements that are fair to providers but also fair to patients and purchasers?

The payer marketplace in MA has been slow to offer transparency and shared savings products to employers and many benefits advisers have continued to favor the status quo. Perhaps the findings of this new report will inspire active change and an employer movement toward value.

Jeffrey Hogan is a healthcare thought leader and regularly appears on national and local forums focused on moving to value based healthcare and is actively working to promote healthcare transparency.